By their economic nature, standard tax deductions are largely a social component and serve as a measure of social support for certain categories of citizens. In this publication N.V. Fimina, a lawyer and tax expert, examines the procedure for an organization to provide standard deductions for personal income tax in some typical situations. 1C company methodologists tell us how, in accordance with the given recommendations, calculate the amounts of personal income tax payable to the budget in an automated mode using the 1C: Salary and Personnel Management 8 program.

The current legislation of the Russian Federation distinguishes two types of standard deductions for personal income tax.

Firstly, a deduction for the citizen himself (personal deduction) - in the amount of 3,000, 500 rubles. (Subclause 1-2, Clause 1, Article 218 of the Tax Code of the Russian Federation). This deduction is not provided to all individuals, but only to some (Chernobyl survivors, veterans, disabled people of groups I and II, etc.). A complete list of cases of providing personal standard tax deductions for personal income tax is given in Table 1.

Table 1

Standard deductions not related to the presence of children*

|

Deduction amount |

A comment |

|

|

Persons affected by radiation |

Related to the radiation impact of the disaster at the Chernobyl Nuclear Power Plant (ChNPP); |

|

|

The following have the right to a deduction in the specified amount: |

||

|

Disabled people |

Disabled persons of the Great Patriotic War (WWII), as well as Disabled military personnel who became disabled in groups I, II and III during the performance and duties of military service; Disabled former partisans, as well as other categories of disabled people who are equal in pension benefits to the specified categories of military personnel. |

|

|

Disabled people since childhood, as well as disabled people of groups I and II have the right to a deduction in the specified amount |

||

|

Persons who took part in hostilities |

The following have the right to a deduction in the specified amount: |

|

|

Persons who donated bone marrow to save lives |

A document confirming the right to a deduction can be a certificate from a medical institution confirming bone marrow donation (letter of the Ministry of Finance of Russia dated December 15, 2010 No. 03-04-06/7-302). |

|

|

Parents and spouses of fallen military personnel and government employees |

The following have the right to a deduction in the specified amount: For example, the parents of a serviceman who died while performing military service in a combat area in the Chechen Republic are entitled to receive a standard tax deduction in the amount of 500 rubles. for each month of the tax period (letter of the Federal Tax Service for Moscow dated September 11, 2006 No. 28-11/80630). |

* See paragraph 1 of Article 218 of the Tax Code of the Russian Federation. If an individual is simultaneously entitled to several of the deductions indicated in the table, one of these deductions is provided.

Secondly, citizens with children, spouses of parents, adoptive parents, guardians, trustees, and adoptive parents are entitled to standard deductions. The deduction is provided for each child under 18 years of age. And also for children under the age of 24, if they are full-time students, graduate students, residents, interns, students, cadets (subclause 4, clause 1, article 218 of the Tax Code of the Russian Federation).

- 1,400 rub. per month - for the first child (deduction code - 114*);

- 1,400 rub. per month - for the second child (deduction code - 115);

- 3,000 rub. per month - for the third and each subsequent child (deduction code - 116);

- 3,000 rub. per month - for each disabled child under the age of 18 (deduction code - 117);

- 3,000 rub. per month - for each disabled child of group I or II under the age of 24, if the child is a full-time student (student, graduate student, resident, intern) (deduction code - 117).

Note:

*hereinafter in the text the deduction codes from the reference book “Deduction Codes” are indicated in accordance with Appendix No. 3 to the order of the Federal Tax Service of Russia dated November 17, 2010 No. ММВ-7-3/611@ (as amended by the order of the Federal Tax Service of Russia dated December 6, 2011 No. ММВ- 7-3/909@).

The standard child tax deduction must be provided in double amount:

- the only adoptive parent;

In this case, deduction codes 118, 119, 120, 121 are used (depending on whether the deduction is provided for the first, second, third child, disabled child or student over 18 years of age).

The current legislation of the Russian Federation also provides for the possibility of one parent (adoptive parent) refusing the deduction in favor of the other (see further section of the article “An application has been received for the refusal of the employee’s spouse to deduct”). In this case, deduction codes 122, 123, 124, 125 are used, depending on whether the deduction is provided for the first, second, third child, disabled child or student over 18 years of age.

A tax deduction for a child is provided until the income of the taxpayer-employee, calculated on an accrual basis from the beginning of the tax period - the calendar year - reaches 280,000 rubles. (Article 218 of the Tax Code of the Russian Federation).

A distinctive feature of standard tax deductions is the ability to provide them to one individual on several grounds at once.

In the 1C: Salaries and Personnel Management 8 program, standard tax deductions are stored in the directory Salary calculations -> Directories -> Personal income tax deductions(Fig. 1). Let's consider several situations related to providing citizens with standard tax deductions for personal income tax, which often raise questions among practitioners.

Rice. 1

The deduction is not applied from the beginning of the year

Correct application of standard tax deductions for personal income tax is impossible without answering the questions from when to apply deductions:

- year to date;

- from the date of hire;

- from the month of receipt of the application for deduction.

In letter dated 08.08.2011 No. 03-04-05/1-551, the Ministry of Finance of Russia explained that standard tax deductions for personal income tax are provided to the taxpayer by one of the tax agents who are the source of payment of income, at the taxpayer’s choice based on his written application and documents confirming the right to such tax deductions (clause 3 of Article 218 of the Tax Code of the Russian Federation). If the taxpayer's eligibility for the standard tax deduction has not changed, there is no need to reapply.

Thus, if we are talking about continuing to provide a personal deduction or a deduction for a child under 18 years of age, the tax deduction is applied starting from January of the current year without additional documents. This rule applies if other deduction conditions are met. In particular, regarding the child deduction, we are talking about the following conditions: the child’s age is less than 18 years and the taxpayer’s income since the beginning of the year has not exceeded 280,000 rubles.

If we are talking about a deduction for a child under 24 years of age who is studying full-time, we recommend that in order to provide a deduction from January, you additionally request at the beginning of the year a certificate from the educational institution confirming that the child is still enrolled in this educational institution (see the section of this article for more details " The employee’s child did not pass the test”).

If an employee is hired in the middle of the year, deductions should be provided from the month of hire. At the same time, in order to correctly provide a deduction for a child, a certificate from the previous tax agent will be required: a deduction for a child is provided until the income, calculated cumulatively from the beginning of the year, does not exceed 280,000 rubles. (paragraph 17, subparagraph 4, paragraph 1, article 218 of the Tax Code of the Russian Federation).

2-NDFL certificates must be presented from all previous places of work from the beginning of the tax period (calendar year).

In the 1C: Salaries and Personnel Management 8 program, a certificate from the previous place of work must be entered into the directory form Individuals by clicking on the button Personal income tax To Data entry for personal income tax on the bookmark Income from previous jobs(Fig. 2).

Rice. 2

Here in the field Organization data the organization in which this certificate will be taken into account is indicated if the employee works in several organizations. If he is accepted into only one company, then its name will be substituted by default.

Quite often, practicing specialists have a question: is it possible to provide a standard deduction if the employee does not have a certificate in Form 2-NDFL from the previous employer. In such a situation, a deduction is possible only if the person has not worked since the beginning of the year. This fact can be confirmed, for example, by a copy of the work record book.

Otherwise, the following must be considered. One of the documents that confirms an employee’s right to a tax deduction for a child (if he did not start working in the organization from the beginning of the year) is a certificate in form 2-NDFL from the previous employer.

If there is no certificate, then the employer does not have the right to provide such a deduction to the employee (see, for example, resolutions of the Federal Antimonopoly Service of the Volga Region dated 09.10.2008 No. A12-55/08, West Siberian District dated 05.12.2006 No. F04-7924/2006(28822- A46-27), dated July 27, 2006 No. F04-4697/2006(24695-A46-27) and dated April 20, 2006 No. F04-1436/2006(21704-A46-7)).

To be fair, it is worth noting that there is arbitration practice confirming the legality of providing deductions without a 2-NDFL certificate from a previous employer (see, for example, resolutions of the Federal Antimonopoly Service of the Moscow District dated March 17, 2009 No. KA-A40/1343-09, dated October 24, 2006 No. KA-A40/10310-06, Northwestern District dated October 30, 2008 No. A56-2606/2008, dated August 14, 2006 No. A05-3035/2006-31, Ural District dated November 7, 2006 No. Ф09-9786/06-С2 and dated 04/14/2005 No. F09-1344/05-AK, Central District dated 10/18/2005 No. A14-2305-2005/70/10 and dated 06/01/2005 No. A54-5096/04 C8). However, following this position is risky; the likelihood of disputes with inspectors is extremely high.

If during the year the employee’s status changed (he had a child or the citizen became disabled), the deduction should be provided from the month of filing the application for the deduction. At the same time, if for some reason the application did not reach the accountant in a timely manner, then during the tax period it is necessary to take this application into account. Recalculation of deductions and personal income tax in the program will occur automatically in the billing period for previous months, starting from the month from which the user sets the application of deductions in the program.

You should indicate the use of deductions in the program in the form of the directory Individuals by clicking on the Personal Income Tax button to Entering data for personal income tax on the Deductions tab (Fig. 3).

Rice. 3

Deductions are applied from the date and in the organization specified in the Application of deductions field. If this field is not filled in, information about the rights to deductions is not reflected when calculating personal income tax.

In the Entitlement to standard deductions for children field, you can specify the expiration date of entitlement. It is recommended to set the date of reaching 18 years of age or the date of the next request for a certificate from the university.

A citizen can fill out an application in any form (see sample application form No. 1).

Application form No. 1

|

To the head of the organization STATEMENT When determining the tax base for personal income tax, I ask you to provide me with the following monthly standard tax deductions from “____”______________201___: 1. In accordance with sub. 2 p. 1 art. 218 of the Tax Code of the Russian Federation in the amount of 500 rubles. I am attaching documents confirming the right to deduction: A copy of the certificate confirming bone marrow donation. 2. In accordance with sub. 4 p. 1 art. 218 of the Tax Code of the Russian Federation in the amount of 3,000 rubles. (for the fourth child - Anna Andreevna Alekseeva, born on August 12, 1999). I am attaching documents confirming the right to deduction: Copies of children's birth certificates: second - Alekseev Ilya Andreevich; third - Evseev Ivan Antonovich; fourth - Alekseeva Anna Andreevna. I am attaching certificates in form 2-NDFL from previous places of work this year. |

The age of the child is important to confirm the parent’s right to receive a deduction for this particular child. The order of birth of children (first, second, third) does not change due to the fact that the eldest child died or reached an age after which standard deductions for him are not provided to parents. He is still the eldest (first), and the remaining children remain, respectively, the second and third child.

A lease agreement has been concluded with an individual

Income received by a citizen under a lease agreement is subject to personal income tax. There are three different situations to consider in this section:

- the tenant is the only tax agent paying income to the citizen (for example, if a lease agreement is concluded with a pensioner);

- the lease agreement was concluded with an employee of the organization;

- the lease agreement is concluded with a person who works in another place under an employment contract.

If the contract is concluded with an individual who does not receive other income in addition to rent, the following must be taken into account. The features of providing standard tax deductions to the lessor are explained in the letter of the Ministry of Finance of Russia dated October 12, 2007 No. 03-04-06-01/353. If during a tax period income to an individual is not paid every month, but, for example, only twice, a standard tax deduction can be provided for all months of the tax period preceding the payment of income, until the income limits are reached, calculated on an accrual basis from the beginning of the tax period, above which standard tax deductions are not provided. Thus, the right to deduction is retained during the tax period - the calendar year. The deduction for the current month and the deduction for the previous month (when the person did not receive income) are summed up.

If the contract is concluded with an employee of the organization, deductions are not provided separately under the contract.

Example 1

Let us consider sequentially the procedure for reflecting these events in accounting in “1C: Salary and Personnel Management 8”. To hire an employee in the program, you can use the Hiring Assistant or the Hiring document.

You can enter information about standard tax deductions either from the directory Individuals(menu Enterprise -> Individuals), or from the directory Employees(menu Enterprise -> Employees). Information about standard tax deductions is indicated in the program in the form Entering data for personal income tax(menu Enterprise -> Employees-> section Tax deductions, Taxpayer status-> field Standard) or by clicking on the personal income tax button from the directory Individuals.

Document Entering data for personal income tax consists of several parts. Part in this case it is not filled in. The employee did not provide documents confirming his right to a personal deduction of 3,000 rubles. or 500 rub. (is not a disabled person, a person affected by radiation, etc.)

You can display in the program the data on the deduction that is provided to Ivanov as follows. On the bookmark Deductions in the tabular section Eligibility for the standard deduction for children a new line is entered using the button Add. In props Period from the date indicated - 01/01/2013. From January, the employee has the right to a deduction.

Let's take a closer look at the procedure for specifying the end date of the deduction. The limit determining the age of the child, upon reaching which the parent loses the right to deduction, is established by paragraph 12 of paragraph 4 of Article 218 of the Tax Code of the Russian Federation - 18 years or 24 years - if the child is a full-time student, graduate student, resident, intern, student or cadet. In this case, the employee’s child is 10 years old and it is unknown where he will study after school. Therefore, we apply the first of the specified age criteria - 18 years. As a general rule, the deduction is provided until the end of the calendar year in which the child reaches 18 years of age. This procedure is provided for in paragraphs 11 and 12 of subparagraph 4 of paragraph 1 of Article 218 of the Tax Code of the Russian Federation. Therefore, the end date for the provision of deductions is December 31, 2021.

In props Code and number of children the fact that an individual has the right to the corresponding type of deduction was recorded ( Apply or Do not apply), in the other two columns - the deduction code that is applied and provided to this employee depending on the priority of the child and the number of children dependent on the employee, for whose maintenance a deduction with the specified code should be provided. In our example, code 114/108 is for the first child and the number of children is 1.

In props Base The document on the basis of which the standard deduction is provided is indicated. In our example, a birth certificate.

In order for standard tax deductions, the right to which is reflected in the upper part of the form, to be provided when calculating personal income tax, you must enter data in the tabular section Application of deductions. By button Add data on the use of deductions is filled in automatically. After filing standard deductions for a child in the manner described above, when Ivanov’s monthly wages (other taxable income) are calculated, personal income tax will be calculated using a deduction of 1,400 rubles. per month (until the employee’s income, calculated cumulatively from the beginning of the year, reaches 280,000 rubles).

In April 2013, deductions to Ivanov will be provided as follows. First, his total income for the month will be calculated. Provided that the month is fully worked out, income subject to personal income tax will be equal to: 30,000 rubles. + 10,000 rub. = 40,000 rub. The personal income tax amount will be:

(40,000 rubles - 1,400 rubles) x 13% = 5,018 rubles.

The deduction does not apply separately to income in the form of rent.

Let's consider another situation:

Example 2

To establish specific reasons for the provision of standard tax deductions to an individual by two or more tax agents during one tax period, and also to identify, as possible consequences, the fact that a person committed a tax offense, which resulted in the incomplete payment of personal income tax by this individual, or the fact that a tax agent failed to fulfill his obligation to The tax authority has the right to withhold and transfer tax to the budget during tax control through tax audits and receive explanations from taxpayers and tax agents. As experts from the regional Federal Tax Service emphasize, both a citizen and a tax agent can be found guilty of such an offense (see, for example, http://www.r59.nalog.ru/ fl/fl_ndfl/fl_nal_v/standvich59/3712169/).

An employee has been assigned a disability

A disabled person is considered to be a person who has a health impairment with a persistent disorder of body functions, caused by diseases, consequences of injuries or defects, leading to a limitation of life activity and causing the need for his social protection (Part 1 of Article 1 of the Federal Law of November 24, 1995 No. 181-FZ) . Recognition of a citizen as a disabled person is carried out during a medical and social examination in the manner established by Decree of the Government of the Russian Federation of February 20, 2006 No. 95 “On the procedure and conditions for recognizing a person as disabled.” A citizen recognized as disabled is issued a certificate confirming the fact of disability, indicating the group, as well as an individual rehabilitation program.

From the month in which a person received a disability of group I or II, he can take advantage of the right to a standard tax deduction for personal income tax in the amount of 500 rubles. (subject to providing the employer with a certificate and an application for a deduction). The current legislation of the Russian Federation does not provide for norms on the maximum amount of income limiting the right to this deduction. The deduction should be provided regardless of the amount of income.

Example 3

In the 1C: Salary and Personnel Management 8 program, information about the standard personal deduction should be reflected in the form Entering data for personal income tax(menu Enterprise -> Employees -> section Tax deductions, Taxpayer status-> field Standard) in the following way. On the bookmark Deductions in the tabular section Eligibility for personal standard deduction a new line is entered using the button Add. In props date The date indicated is 02/01/2013.

In props Code code 104 is indicated (disabled person of group II). In props Base- a document on the basis of which a standard deduction is provided - a certificate of disability.

It should be noted that filling out the details Base is not mandatory. Relevant information is indicated if necessary to optimize the search for documents (for example, in the case of an audit by tax inspectors).

The disability group may be revised. For example, an employee with a disability of group II, who received a deduction of 500 rubles during the year, ceases to receive a deduction after the disability group is revised (assigning a disability of group III).

Filling in the details Base will allow the accountant to monitor this issue in the future and timely request from the employee a document confirming the right to deduction.

Next by button Add the lower section of the document is filled with data Application of deductions. If the data on the use of deductions is not filled out, then, despite the fact that information on the right to deductions has been entered, deductions will not be provided.

The newly hired employee is the only parent

As we indicated above, the deduction for a child should be provided in double amount:

- unmarried single parent (adoptive parent);

- the only adoptive parent;

- the sole guardian (trustee).

The status of “single mother” is not always identical to the status of “single parent”.

If a new employee asks for double the standard child deduction, here are some things to keep in mind.

A parent (guardian, trustee) is recognized as the only one if:

- the second parent (guardian, trustee) died;

- the second parent (guardian, trustee) is recognized by the court as missing or deceased;

- the father is not indicated on the child’s birth certificate;

- the paternity of the child has not been legally established;

- The guardianship and trusteeship authority has appointed only one guardian (trustee) for the child.

Is not the only parent, in particular:

- mother or father who had a child outside of a registered marriage, if paternity has been established;

- mother or father of the child, if one of the parents is deprived of parental rights;

- a single parent (if he is not the only one), regardless of whether he is married or not, whether the child is adopted or not by the spouse in a new marriage.

Thus, the fact that a woman gave birth to a child without being in a registered marriage does not affect the procedure for granting the deduction.

To confirm the right to a standard double tax deduction, the only parent must provide a copy of the child's birth certificate, a copy of the passport, and other supporting documents (see table 2).

table 2

Documents confirming the right to a standard personal income tax deduction for a child in double amount*

|

No. |

Situation |

A document confirming the right to a double deduction |

A comment |

|

Second parent died |

Copy of the death certificate of the second parent |

There is no need to notarize the copy |

|

|

The second parent is declared missing or deceased |

Extract from the court decision recognizing the second parent as missing or deceased |

A citizen is recognized as missing at the request of interested parties by the court in the manner prescribed by Chapter 30 of the Code of Civil Procedure of the Russian Federation (Articles 276-280). The condition is the absence at the citizen’s place of residence of information about his place of stay during the year. The condition for recognizing a citizen as dead (clauses 1 and 2 of Article 45 of the Civil Code of the Russian Federation) is the absence at his place of residence of information about his place of stay for 5 years. The legislation also establishes special deadlines: |

|

|

Paternity has not been established |

A copy of the child’s birth certificate, which does not contain information about the child’s father (a dash is placed in the corresponding column). A certificate of the birth of a child, drawn up from the words of the mother at her request (is the basis for entering information about the father into the birth certificate). |

For children born before 1999, instead of a certificate, another similar document issued by the Civil Registry Office must be submitted |

|

|

The child is assigned a sole guardian or trustee |

Act of the guardianship and trusteeship authority on the appointment of a guardian or trustee |

If the guardian or trustee marries, the standard deduction does not change and remains double. This is explained by the fact that spouses of guardians or trustees are not entitled to deductions in relation to children under their care. In other words, guardians and conservators do not “pass on” one of their two deductions to their spouses. At the same time, as an exception to the general norm, the guardianship and trusteeship authority, when placing children without parental care in a family, based on the interests of the child, may appoint several guardians or trustees. In this case, the right to standard deductions arises for each of them, but only in a one-time amount. Similar explanations can be found on the websites of regional Federal Tax Service (see, for example, http://www.r59.nalog.ru/fl/fl_ndfl/fl_nal_v/standvich59/3888265/). |

Note:

* See letters of the Ministry of Finance of Russia dated July 19, 2012 No. 03-04-06/8-206, dated May 23, 2012 No. 03-04-05/1-657, dated August 12, 2010 No. 03-04-05/5-449 .

The fact that parents are divorced or the deprivation of one of the parents of parental rights does not mean that the child does not have a second parent, that is, the child has a single parent, therefore, if one of the parents is deprived of parental rights, the other parent does not have the right to receive a double tax deduction established by subparagraph 4 paragraph 1 of article 218 of the Tax Code of the Russian Federation. In this case, the mother cannot be recognized as the only parent, including if the spouses are divorced and the location of the father is not established. The fact that a parent marries, provided that the child is not adopted, does not in any way affect the status of the only parent.

An employee's child failed the exam

Subparagraph 4 of paragraph 1 of Article 218 of the Tax Code of the Russian Federation provides that:

- up to 18 years of age, deductions are provided regardless of whether the child is studying or not;

- up to 24 years of age, deductions are provided if the child is a full-time student (graduate student, resident, intern, student, cadet).

Actually, the very fact of failure to pass the test does not affect the procedure for providing standard deductions for personal income tax for the child. An employee’s child may be transferred to a repeat year of training. He can take an academic leave, during which deductions are provided to the parent in the general manner.

The fact that an employee’s child is expelled from an educational institution has legal consequences. If the child completes his studies before he turns 24 (this also applies to the situation when the child was expelled from the university for some reason), there will no longer be grounds for providing a deduction (letter of the Ministry of Finance of Russia dated October 12, 2010 No. 03-04 -05/7-617). And the parent will lose the right to the deduction starting from the month following the one in which education ceased. For example: if a child has been expelled since June, already in July, and not after the end of the holidays in September, the accountant must reflect in the program the termination of the deduction.

In practice, the following situation is possible: in January, an employee presented a certificate from an educational institution confirming that the child is a full-time student. The accountant provides the deduction until the end of the year and finds out that the child was expelled from the educational institution in June. Personal income tax will have to be withheld from subsequent income. Providing a deduction is illegal.

To avoid this problem, the employer can oblige employees to provide certificates of education for their children twice a year - in January and September.

If a child who has been studying full-time since the beginning of the year transfers to an evening (part-time) department after failing the exams, his parent loses the right to deduction from the beginning of distance learning. However, there is no need to recalculate the tax for periods of full-time study. The use of standard deductions for a child for this period is legal. Similar explanations can be found on the websites of regional tax service departments.

For example, specialists from the Federal Tax Service for the Perm Territory comment on a similar situation. In January - March, the student studied part-time (evening), and from April until the end of the year - full-time. In this case, tax department specialists indicate that parents have the right to receive a standard tax deduction from April onwards.

An application has been received regarding the refusal of the employee’s spouse to waive the deduction.

A double deduction can be provided to one of the parents (adoptive parents) of their choice, if the second parent (adoptive parent) refused the deduction in writing (paragraph 16, subparagraph 4, paragraph 1, article 218 of the Tax Code of the Russian Federation). If the employee’s spouse is not the child’s parent (for example: we are talking about a child from a previous marriage), there is no need to accept documents for waiver of the deduction and provide a double deduction. This section will discuss the situation when the employee’s spouse, who is the second parent of the child, refuses the deduction.

For the documents required to provide a double deduction, see Table 3.

Table 3

Registration of a waiver of the standard deduction for a child in favor of the second parent

|

Who draws up the document |

Title of the document |

ATTENTION: similar article on 1C ZUP 2.5 -

Hello dear site visitors. Today in the next article we will talk about how in the program 1C 8.3 ZUP 3.1 The process of accounting for various types of personal income tax has been organized:

- Calculated personal income tax

- Withheld personal income tax

- Listed personal income tax

We will look in detail at what documents these types of personal income tax are taken into account and in what registers they are reflected. Let's look at a specific example of how to register in a program employee's right to receive a standard tax deduction and how it will be taken into account when calculating personal income tax. Let's consider some other settings that must be taken into account for the correct calculation of personal income tax in the 1C ZUP program, edition 3.

✅

✅

First we'll talk about calculated personal income tax. In the ZUP 3.0 (3.1) program, this personal income tax is calculated in the documents “Accrual of salaries and contributions”, as well as in various inter-account documents, such as “Vacation”, “Business trip”, “Sick leave”, “Bonuses”, “One-time accruals” and in some others. First, let's talk about how it is calculated Personal income tax in interpayment documents. I will analyze today’s material on the basis of the information base that we have formed as a result of previous publications, where I talked about and.

Let's look at the inter-account document “Sick leave” for employee A.M. Ivanov. for October. This document is a personnel accounting document and when filled out, the program automatically determines the employee’s average earnings for the two calendar years preceding the year of temporary disability. Here, sick leave is completely calculated based on average earnings, and is calculated by personal income tax. You can view the details of the calculation of this tax by clicking on the button with the image of a green pencil.

In the window that opens “More details about personal income tax calculation” we will see the amount of calculated tax, date of receipt of income, for which it is calculated, possible standard and property deductions, if they are registered for the employee. In our example, Ivanov A.M. There are currently no personal income tax deductions. Personal income tax was calculated correctly - 252 rubles, which is 13% of the amount of income of 1,935.49 rubles.

I would like to pay special attention to the props "payment date" in the document “Sick leave”. The fact is that it is very important to correctly indicate this date in interpayment documents. For incomes for which the income code is NOT equal to code 2000 or 2530 (and for hospital income code 2300), it is according to "payment date" determined "date of receipt of income", and this date determines which month of the tax period the income and the personal income tax calculated from it will be attributed to.

In the document “Sick leave” the date of payment is indicated 05.11 (payment with salary) and based on it was automatically filled in date of receipt of income Also 05.11 , which is what we actually see in the “More details about personal income tax calculation” window. Accordingly, we will have the month of the tax period for personal income tax accounting purposes November. Where can we see this period? For example, if according to employee Ivanov A.M. generate a “Certificate of Income (2-NDFL)”, it will be seen that income with code 2300 (and these are sick leave, in the amount of 1,935.49 rubles for our example) fell in the month of the tax period November. The same thing will happen in the regulated report “2-NDFL for transfer to the Federal Tax Service” if we generate it.

It should also be said that the date of receipt of income, which will be determined for the calculated personal income tax in the intersettlement document, directly affects the completion of the quarterly report 6-NDFL. I discuss the issue of filling out 6-NDFL in 1C ZUP 3.0 (3.1) in great detail in the article

So this sick leave in tax accounting was registered in November. We are convinced of this. But it is worth noting that the accrual month in the “Sick Leave” document is indicated as October. This means that if we generate salary reports in the program from the Salary (Salary Reports) section, such as “Payslip”, “Full set of accruals, deductions and payments” or “Salary analysis for employees (as a whole for the period)” , then in them this sick leave will be attributed to the month October. Let's look at the example of Salary Analysis for Employees, indicate the period from 01.10 to 31.10 and see that sick leave is included in the report.

Those. there is a difference between what month of the tax period this income is registered (NOVEMBER), and to which month of accrual, he is assigned (OCTOBER). It is worth understanding this difference and keeping in mind that this situation is normal.

Registration of calculated personal income tax with the document “Accrual of salaries and contributions” in 1C ZUP 3.1 (3.0)

Now let's look at the document "Calculation of salaries and contributions" for October. Here, personal income tax is also calculated (the “personal income tax” tab), and the screen below shows that in this example, personal income tax is calculated exactly from the employee income that is accrued in this document. But in fact, the program analyzes all employee income from the beginning of the year, i.e. Personal income tax is calculated on an accrual basis from the beginning of the year. If the program sees that for some reason the tax was not calculated in interpayment documents or in previous months, but should have been, then this personal income tax will be calculated here, i.e. The program will not lose any income.

To illustrate this point, let’s remove the personal income tax in the Sick Leave document and assume that for some reason it was not calculated. Let's spend sick leave in this form.

Now, let’s recalculate personal income tax in the document “Calculation of salaries and contributions.”

Please note that according to employee Ivanov A.M. in the document “Calculation of salaries and contributions” on the personal income tax tab, we now have two lines formed. In the first line, 1857 rubles. - this is the calculated tax on salary payment in the amount of 14,285.71 rubles. The second line, 252 rubles, is the tax calculated from sick leave and we can determine this by the date of receipt of income 05.11, which corresponds to the date of payment in the “Sick Leave” document.

Thus, the date of receipt of income will be the last day of the month for which it was accrued, i.e. 31.10.

The same goes for other employees. Sidorov S.A. in October, payment was accrued at an hourly rate and a percentage bonus; these types of accrual also have an income code of 2000, respectively, the date of receipt of income is the last day of the month - 10/31.

Employee Petrov N.S. in October, payment was accrued based on salary (by the hour) and payment for work on holidays and weekends, these types of accrual also have an income code of 2000, respectively, the date of receipt of income is the last day of the month - 10/31

Thus, the date of receipt of income is determined in accordance with the income code specified in the accrual type settings. For income with code 2000.2530 “date of receipt of income” is defined as the last day of the month, for which income is accrued, and for other income - by date of payment of income.

For clarity, we will also create a “Vacation” document for employee S.A. Smirnov. If we look at the details of the calculation of this personal income tax, we will see that the “date of receipt of income” was also determined by the “date of payment” specified in the document - 07.11

Therefore, I would like to draw your attention once again to the fact that very important correctly indicate the date of payment of income in interpayment documents. In the document “Accrual of salaries and contributions”, the date of payment does not need to be indicated, since the program automatically determines the date of receipt of income based on the month for which income is accrued and sets the last day of this month.

Let's look again at the “Certificate of Income (2NDFL)” for employee A.M. Ivanov. Here we see that income code 2000 (salary payment) in the amount of 1,4285.71 rubles is assigned to the month of the tax period October, and income code 2300 (Sick leave) in the amount of 1,935.49 rubles - November. But in the salary report “Analysis of salaries by employees” for the period from 01.10 to 31.10, both Salary and Sick Leave are indicated.

I would also like to talk about the technical side of this issue, i.e. tell us in which registers in the 1C ZUP 3.0 (3.1) program it is taken into account counted Personal income tax (by the way, I have already discussed this issue in some detail in the article). So, in order for us to view these registers, it is enough to open the document “Accrual of salaries and contributions”, i.e. the document in which this personal income tax was calculated and directly into the form of this document display all those registers on which this document can make movements. To do this, open the Main menu – View – Setting up the form navigation panel. In the “Available commands” field, select the register we need, it is called “”, and it is taken into account counted Personal income tax, click the “Add” button and this register will go to the “Selected commands” field. Click OK.

A link will appear at the top of the “Payroll and Contributions” document “Calculations of taxpayers with the budget for personal income tax”, when opened, you can view the movement of this document in this register. In the register Calculations of taxpayers with the budget for personal income tax 4 entries occurred, exactly those that are present on the personal income tax tab in the “Calculation of salaries and contributions” document.

I want to draw your attention to the fact that this movement is done with a plus sign, that is incoming movement, and means that this counted Personal income tax. An expense movement with a minus sign in this register is withheld personal income tax. We'll talk about it further.

Registration of withheld personal income tax with the documents “Vedomost...” in 1C ZUP 3.1 (3.0)

✅

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Firstly, it is worth noting that in the 1C ZUP 3.1 (3.0) program registration withheld personal income tax carried out in the documents “Vedomost...”:

- "Statement to the bank"

- “Statement of transfers to accounts”,

- "Statement to the cash register"

- “Payment sheet through the distributor.”

For our example, we will create the document “Statement to the Bank”. The program will automatically fill out the document with those employees whose payment method is assigned in the organization’s settings, i.e. by crediting to the card within the framework of a salary project (in our example, these are employees A.M. Ivanov and N.S. Petrov). You can read more about paying advances and salaries in 1C ZUP in the article.

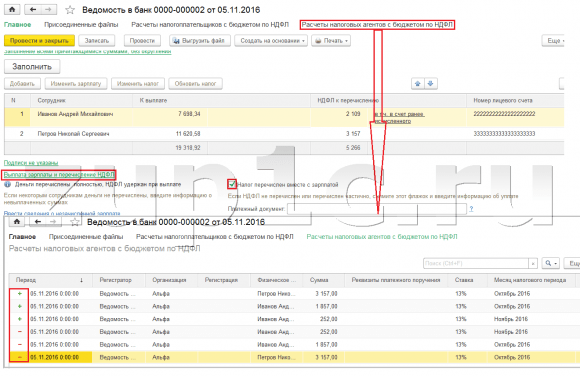

When filling out this document, the program analyzes not only the balance of debt to the employee (the “Payable” column) and not only indicates the amount to be paid, but also fills out the “Personal Income Tax to be Transferred” column, i.e. the tax that will be withheld when processing the document. When filling this column, the program analyzes the remainder by register “Calculations of taxpayers with the budget for personal income tax”, is there in this register counted, but also unrestrained tax. Therefore, if for some reason personal income tax for the previous months was not reflected as withheld, then the program will take it into account the next time you fill out the “Vedomost...” document.

Now let’s look in more detail at what it was made up of by employee A.M. Ivanov. To do this, double-click on the amount of 2,109 in the “Personal Income Tax to be transferred” column. The “Editing Employee Personal Income Tax” window will open, where we see personal income tax in the amount of 1,857 rubles. from income from salary (date of receipt of income 10/31) based on the document “Accrual of salaries and contributions” and personal income tax in the amount of 252 rubles from sick leave (date of receipt of income 05/11) based on the document “Sick Leave”.

Next, let’s see what movements the document “Statement to the Bank” will make according to the register. For ease of viewing, we will display a link to this register directly in the document form. In exactly the same way as we did in the document “Calculation of salaries and contributions” (Main menu - View – Setting up the form navigation panel). So let's follow the link “Calculations of taxpayers with the budget for personal income tax.” Now we see that, unlike the document “Calculation of salaries and contributions” (receipt movement with a plus sign), the document “Statement to the bank” does consumable movement with a minus sign. It is the expense movement in this register that reflects the fact withholding personal income tax.

Here it is immediately worth noting that it is precisely based on the expense movements of this register that section 2 in the report “6 Personal Income Tax” is formed (more details in the article). And in this regard very important so that the retention period (date) is indicated correctly. In fact, this is line 110 in section 2 of the “6 personal income tax” report. The retention date (period) in the register is filled in automatically in accordance with the date specified in the “Statement...” document. Therefore, once again I draw your attention, very important To correctly fill out section 2 of report 6 of personal income tax, correctly indicate the date in the document “Statement...”, i.e. exactly the date when wages are actually paid and personal income tax is withheld accordingly.

Registration of the listed personal income tax with the documents “Vedomost...” in 1C ZUP 3.1 (3.0)

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

In the 1C program ZUP 3.1 (3.0) personal income tax listed, as well as withheld, are registered by default in the “Vedomost...” documents. Let's look at the listed tax using the example of the document “Statement to the Bank”. If we follow the link Payment of salaries and transfer of personal income tax, which is located at the bottom of the document, then some more details of this document will open. By default, this checkbox is checked Tax is transferred with salary and that is why the document “Gazette …” registers the fact of personal income tax transfer. In the payment document field, we can immediately indicate the number and date of the payment document by which the personal income tax was transferred.

Now let's talk about registers. Listed personal income tax reflected in the register. Let's display a link to the register Calculations of tax agents with the personal income tax budget to the form of the document Statement to the Bank (Main menu – View – Setting up the form navigation panel) and see its contents. In this register income movement with plus now registers fact retention Personal income tax, and with a minus - consumable movement registers listed tax.

Now let's talk about an alternative way of registering the fact of transferring personal income tax to the budget. If we do not want to reflect the fact of personal income tax transfer in the “Vedomosti...” document itself, then the program contains a document “Transfer of personal income tax to the budget”. But why might we not want this?

In this situation, if we reflect the transfer of personal income tax in the document “Sheet ...”, then in fact in the program this transfer is registered on the date that appears in the Sheet itself, i.e. in our example, the fact of transfer was registered on the date 05.11. If we actually transferred this personal income tax the next day, i.e. 6.11 (we have the right to transfer personal income tax no later than the next day after payment of wages, and personal income tax from sick leave and vacation pay no later than the end of the month), and not 5.11, then it turns out that we store not entirely reliable information in the program. Therefore, for more correct accounting, this listing should be reflected in 6.11.

But, nevertheless, I will show how to reflect the transfer of tax in a document “Transfer of personal income tax to the budget”.

Let’s uncheck the checkbox in the “Statement to the Bank” document “The tax is transferred along with the salary” and we will make a statement. Let's follow the link Calculation of tax agents with the personal income tax budget and we will see that now the document only does income movement with a plus sign, i.e. registers only held Personal income tax, but the one listed was not recorded.

Next, please note that a new link has appeared in the document “Statement to the Bank” Enter personal income tax transfer data. Let's use it, and the program will transfer us to the document log Transfer of personal income tax to the budget. Let's create a new document. We will transfer the tax on 06.11. In the Amount field, we will enter the amount of tax that is indicated in the document Statement to the bank in the column “Personal income tax to be transferred” in the amount of 5,266 rubles, i.e. We will remit any tax withheld on this statement. Click the spend button.

The program begins to analyze the register Calculations of taxpayers with the budget for personal income tax in the document “Statement to the Bank”. She sees that there is an incoming movement of the withheld tax, but there is no outgoing movement of the transferred tax. That is, there is a remainder in this register. The amount of 5,266 rubles is distributed in proportions between all these balances (by Employee and Date of receipt of income) and is formed consumable movement, i.e. fact of personal income tax transfer. Accordingly, we list what is withheld. You can compare. Let's open the register Calculations of taxpayers with the budget for personal income tax in the document “Statement to the Bank” and in the document “Transfer of personal income tax to the budget”. That's right, all the tax has now been transferred to us.

So, we've run out of lengthy questions. We have sorted out which documents are in the program 1C ZUP 3.0 (3.1) registered calculated, withheld and transferred tax, as well as in which registers these taxes are recorded. Now we will talk about tax deductions for personal income tax. We considered the examples given above without taking into account tax deductions.

Registration of an employee’s right to provide a standard tax deduction in the 1C ZUP 3.1 (3.0) program

The tax base is determined as the amount of income minus the amount of tax deductions provided. There are five types of tax deductions:

- Standard

- Property

- Professional

- Social

- For partially taxable income

In today's article we will talk about how to register an employee's right to provide a standard deduction in the program. Let’s go to the “Taxes and Contributions” section in the “Application for Deductions” journal. Let's open it, here we can create documents such as an application for deductions for personal income tax, Cancellation of standard deductions for personal income tax, Notification of non-commercial organizations about the right to deductions. Let's create a document “Application for personal income tax deductions”. The deduction is provided to employee Petrov N.S., we indicate the date of the document - 01.11, the month from which this deduction will be applied November. Click the “Add” button and from the list of types of personal income tax deductions proposed by the program, select deduction with code 114 (for the first child under the age of 18, for a full-time student, graduate student, resident, student, cadet, under the age of 24). We indicate the month until which the deduction is provided - December. We carry out the document.

Also in the program, we can view information about the deductions provided directly in the employee’s card (section Personnel - Employees directory). Let’s open N.S. Petrov’s card. and follow the link "Income tax". A window will open where we will see the deduction provided to this employee, which we just entered in the document "Application for deductions." If we need to change something in the application, we can follow the link “Correct the application for standard deductions” directly from the employee’s card.

Now let's go to the link Income from previous place of work, In the tabular section, you should indicate the employee’s income from his previous place of work, if he has been working in our organization for more than a year and worked somewhere else this year. This information is necessary for the program to track excess income for the year for the purposes of accounting for deductions, i.e. stopped providing the deduction in a timely manner if the income was exceeded.

Also in this window there is a field where the taxpayer status is indicated. I did not mention this right away in order to present material about where and how various types of personal income tax are registered and proceeded from the fact that all our employees have taxpayer status - Resident(13%, personal income tax is considered a cumulative total). However, the program supports personal income tax accounting for employees with other taxpayer statuses, such as non-residents, highly qualified foreign specialists and others. And this status is selected for the employee here. Depending on the selected status, the tax rate and the algorithm for calculating personal income tax are determined. But this is a topic for other publications.

So, all the necessary information in the program for providing a tax deduction to employee N.S. Petrov. we have contributed, and now we just have to see how it will be taken into account when calculating personal income tax. We will generate a document “Calculation of salaries and contributions” for November. The employee is paid a salary of 30,000 rubles; on the personal income tax tab we see the calculated tax in the amount of 3,718 rubles, taking into account the applied deduction of 1,400 rubles. The calculation will be as follows: (30,000 - 1,400)*0.13 = 3,718 rubles.

In today's article we reviewed quite a lot of material. We talked about where and how to register calculated, withheld and transferred personal income tax. We looked at what tax deductions are provided to employees. Using a specific example, we registered an employee’s right to provide a standard tax deduction.

In the next article I will talk in detail about how contributions are taken into account in 1C ZUP 3.0 (3.1). Follow the publications. All the best!)

To enter information, you need to open the “Individuals” directory, which is located on the “Enterprise” tab.

Or you can go to the “Employees” directory and click on the link “More details and individuals...”.

In the form of the selected individual, click the “Personal Income Tax” button located on the top panel.

A window with three tables opens. In the upper left table, enter information about the right to personal deductions. Until 2012, all employees of the organization were provided with a personal deduction in the amount of 400 rubles (code 103), but it has now been canceled, therefore in this table it is possible to register the right only to provide a monthly deduction of 500 rubles (code 104) or 3000 rubles (code 105 ). However, these deductions are provided only to certain categories of citizens (Heroes of the Soviet Union and the Russian Federation, disabled people of groups I and II, victims during the liquidation of accidents at nuclear facilities, etc.), a complete list of which is contained in Art. 218Tax Code of the Russian Federation.

The top right table records information about eligibility for the standard deduction for children. A new line is added by clicking the "Add" button; you must indicate the period from which the deduction is provided (this can be the date the employee starts working or the date of birth of the child), and the first day of the corresponding month is indicated. You can also indicate the end date of the deduction period (the child reaches a certain age or completes full-time studies at a university), but you can leave this field empty. Information about each child is entered on a new line and each has a separate deduction code (for the third and subsequent children, one line is used, which simply indicates the number of children). The deduction for the first and second child is 1,400 rubles (codes 114 and 115), the deduction for the third and subsequent children is 3,000 rubles (code 116). For example, for an employee with four children, the table will be filled out as follows (in this case, deductions are provided for all children).

Also, separate codes are provided for double deductions (to a single parent, etc.), a list of codes with a description is available for selection in this table.

It is also necessary to fill out the bottom table of this form. It indicates which organization the deductions should apply to. This information is necessary in the case when an employee works simultaneously in several companies or leaves one organization and gets a job in another. But even if you keep records for only one organization, this information must still be provided, otherwise deductions will not be applied.

Deductions are provided for children until the cumulative taxable annual income does not exceed 280 thousand rubles. You can view information about the current amount of income in the employee’s payslip, which is located on the “Payroll” tab. Here you can also see information about the amount of deductions applied in the selected month.

Hello dear blog readers. We started a detailed conversation about personal income tax accounting in 1C ZUP and looked at the simplest example, which presented the full cycle of personal income tax accounting (by the way, you can read about the formation of 6-personal income tax in the article). In that example, personal income tax was calculated using the “Payroll” document. Today I will tell you in what other documents it is possible to calculate personal income tax, and we will also talk about what parameters are available in the 1C Salary and Personnel Management program for setting up personal income tax accounting, why they are needed and where they are located. In particular, we will discuss personal income tax deduction settings, as well as possible options for choosing the status of an individual for personal income tax accounting purposes ( resident, non-resident, highly qualified foreign specialist and others). In this article we will look at two examples:

- In the first one, we will work with the deduction settings - the employee has 4 deductions;

- In the second example, let's see how the program reflects and compensates for excessively withheld personal income tax when the taxpayer's status changes.

✅

✅

So, in the previous publication an example was presented where an employee had only one planned type of accrual, which was calculated in the document "Payroll" and personal income tax from this accrual was also calculated in the same document. But in 1C ZUP there are also a number of accrual documents that provide for the calculation of personal income tax. Let me first list all these documents:

- – “Payment” tab;

- – tab “Calculation of sick leave” -> “Personal income tax”

- – “NDFL” tab

The ability to calculate personal income tax in these documents appeared not so long ago. Previously, personal income tax was calculated only in document "Payroll" and that's why it should have been a last resort so that all accruals for the month are taken into account to correctly calculate personal income tax. This recommendation should still be followed now. Since most of the accrual documents still do not support the independent calculation of personal income tax, the amounts for these documents will be taken into account when calculating personal income tax in the final document “Payroll.” These include the following documents:

- Employee bonuses;

- Registration of downtime of employees of organizations;

- Calculation of severance.

Setting up personal income tax deductions in 1C ZUP

✅

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Now let's talk about how the program sets up accounting for standard tax deductions. First, let me remind you what a tax deduction is. A tax deduction is a certain amount that reduces the tax base, i.e. not subject to personal income tax. In essence, this is a benefit established by the state for a certain circle of citizens. This is where I started talking about standard tax deductions. These include:

- 1400 rub. – for each child (for the first and second child) – code 114/108 (for the first child) and code 115 (for the second child);

- 3000 rub. – for the third and each subsequent child – code 116;

- 3000 rub. – for each disabled child of group I or II – code 117/109;

- 500 rub. - for persons with state awards: in particular, for Heroes of the Soviet Union, Heroes of Russia, for those awarded the Order of Glory of three degrees and many others - code 104 (in the ZUP this deduction is considered a personal standard deduction);

For those who are just starting to get acquainted with the theory of payroll calculation, accounting for personal income tax and deductions, I will give a small example. Let's assume that employee Stepanova has four children, i.e. she has the right to 2 deductions of 1400 rubles each. (code 114 and 115) and 2 deductions of 3000 rubles each. for the third and fourth child (code 116). She also has a salary of 30,000 rubles. Under these conditions, personal income tax (13%) will be calculated using the following formula: (30,000 – (1,400 + 1,400 + 3,000 + 3,000)) * 13% = 21 200 * 13% = 2,756 rub. Thus, the tax base will not be the entire salary, but the amount reduced by the amount of deductions due.

Let's now implement this example in the 1C ZUP program. To fill out information about an employee’s right to standard deductions, the program uses the “Data Entry for Personal Income Tax” form. It can be accessed from the “Employees of the Organization” directory form.

You can also fill in the Reason field, but this is not required. If the Deduction is terminated, the Date and status are indicated "do not apply".

In our example, the employee does not have personal deductions, so we will leave this tabular part empty.

The second tabular part in this form is called "Eligibility for Standard Deduction for Children". We will fill out this form for employee Stepanova. Let me remind you that, according to the conditions of the example, she has four children and, accordingly, can use the following deductions:

- 114/108 – for the first child 1,400 rubles;

- 115 – for the second child 1,400 rubles;

- 116 – for the third and fourth child, 3,000 rubles each. for everyone;

The fields in this tabular section are approximately the same. The only difference is that you can indicate the number of children (we use this option for deduction code 116) and indicate the date until which the deduction is valid, if this is known in advance (we use this for deduction 114/108). You can also stop deduction by entering a separate line, indicating the value “Do not apply”, deduction code and date. The screenshots show both options.

Another tabular part in this form is called "Application of deduction".

And this you need to do it even if you have one organization in the program, otherwise deductions will not be taken into account.

I would also like to draw your attention to the fact that there is another bookmark in this form. Let me remind you that the standard tax deduction is applied until the employee’s cumulative income from the beginning of the year does not exceed 280,000 rubles. Therefore, if an employee does not join the organization from the beginning of the year, then for him you should indicate the income that he had in the previous or previous organization from the beginning of the year. This data will only be taken into account to track the RUB 280,000 limit. These amounts will not affect the calculation of average earnings in any way.

In our case, the employee was hired at the beginning of the year and therefore bookmark “Income from previous jobs” leave it blank.

Taxpayer status for personal income tax

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Taxpayer status in 1C ZUP can be established using the form “Data entry for personal income tax”. It can be opened from the form of the “Employees” directory element in the “Status” field. There are 5 options to select the status:

- Resident

- Non-resident

- Highly qualified foreign specialist

- Participant in the program for the resettlement of compatriots

- Refugee or who has received temporary asylum on the territory of the Russian Federation - appeared in the release of ZUP 2.5.85

There are explanations in the program for each option, so I will only focus on the features of reflecting the situation when an employee’s status changes in the middle of the year. As you can see, in addition to the switches themselves, the form has a field where the period is set. Those. this indicator is periodic. Let's look at a similar situation.

An employee who is a foreign citizen and at the time of hiring (01/10/2014) resides in the Russian Federation is hired by the organization. less than 183 calendar days. Therefore, he is given the status "Non-resident". As a result, personal income tax for January and February is calculated at a rate of 30%.

It turns out that the employee’s personal income tax for January and February is 18,000 = 9,000 + 9,000 = 30,000 * 30% + 30,000 * 30%.

In March, the deadline comes when a foreign citizen’s stay on the territory of the Russian Federation will exceed 183 days. Therefore he acquires the status "Resident". In this case, in 1C it is necessary to change the employee’s status indicating the month in which he received the corresponding status and this will be saved in the history of changes.

As a result, the employee’s personal income tax will begin to be calculated at a rate of 13% from March. But this is not the only change that will occur. When calculating personal income tax for March, the tax for January and February will be recalculated at a rate of 13%. Negative amounts will be calculated for January and February: 30,000 * (13%-30%) = -30,000 * 17% = - 5100; -5,100 *2 = -10,200 rub. (excess withheld for 2 months).

Refunds of excess amounts withheld will be made from the tax calculated in March: RUB 3,900. Those. in March, the employee will receive his full salary without personal income tax withholding. However, personal income tax for March is not enough to fully compensate for the excessively withheld amount and therefore in the payslip for March in the line “including: excessively withheld personal income tax at the end of the period” we will see the figure 6,300 = 10,200 (the amount of excess withheld at the beginning of March) - 3,900 (returned from the March personal income tax).

Please note that this debt in the amount of 6,300 rubles. Although it is listed as a debt for the organization, it will not affect the amount of salary payable. The employee will be paid 30,000, not 36,300.

Thus, the return of excessively withheld personal income tax to the employee will be carried out in the next two months, at the expense of the calculated personal income tax in these months. I hope I explained this mechanism clearly.

In this example, we have a rather simple situation: the employee’s status changed at the beginning of the year and there is time to compensate for personal income tax due to the following months. But it may turn out that the employee changes status, for example, in November and simply there won't be enough time until the end of the year to compensate the entire excess amount withheld. In this case, the program will not carry over this debt to the next year. The employee should independently contact the tax office and it will be the one who will return the excess withheld funds to him. In this case, you should not enter the document "Personal income tax return", since the tax agent (the employer is the tax agent for the payment of personal income tax) does not have the right to return personal income tax to the employee, but can only offset the overpaid amounts against the following months (I talked about this a little higher with an example).

That's all for today!

To be the first to know about new publications, subscribe to my blog updates: